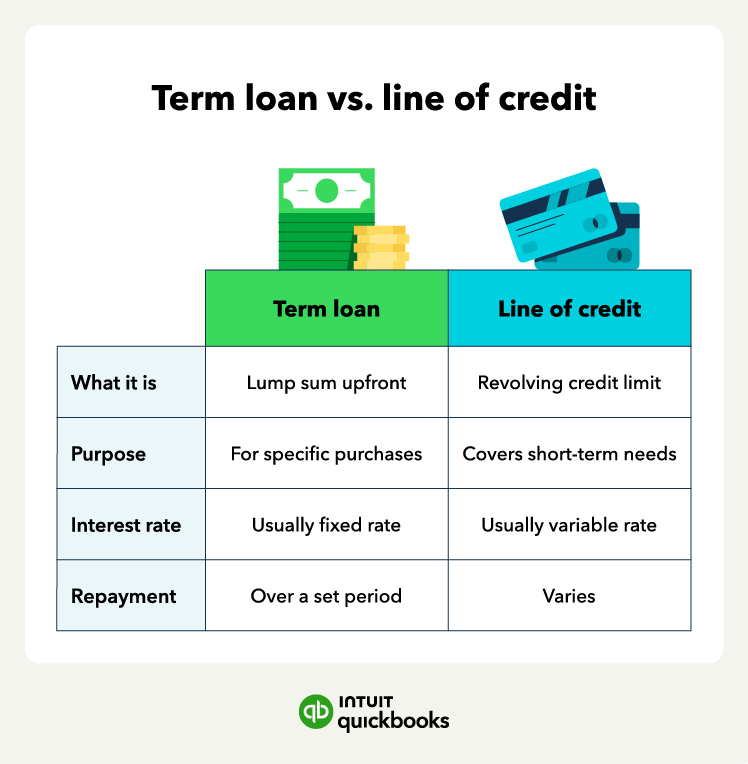

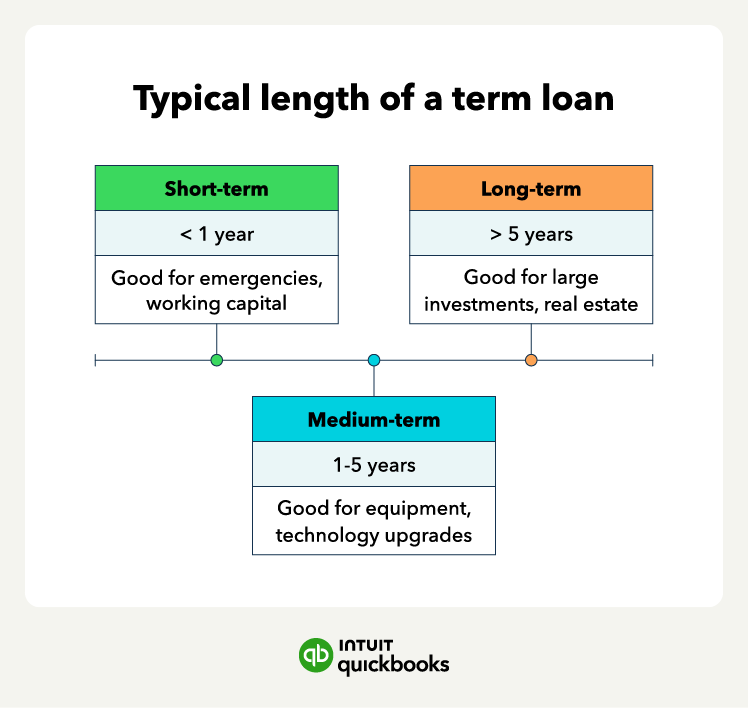

A term loan is a lump sum of money a business borrows from a lender and repays over a set period of time with interest. For many small businesses, term loans are a common way to finance larger, planned expenses, such as purchasing equipment, expanding operations, or managing cash flow during periods of growth.

Revolving credit typically lets you borrow, repay, and borrow again up to a limit, while a term loan typically provides a one-time disbursement repaid in scheduled installments. Business owners evaluating different forms of financing often review a term loan overview alongside other options available through the broader QuickBooks business loans hub to understand how each product fits specific needs.

Jump to:

- What is a term loan?

- How term loans work

- Loan disbursement

- Types of term loans

- Term loan vs. other financing options

- Advantages of term loans

- Disadvantages and considerations

- How to qualify for a term loan

- Interest rates and fees

- Where to get a term loan

- Using term loans effectively

- Term loans and your business plan

- Making your term loan decision